Truist Financial Corporation (TFC) stands as a prominent entity within the highly competitive and dynamic U.S. financial services landscape. Formed from the merger of BB&T and SunTrust Banks, Truist represents one of the largest commercial banking organizations in the United States, providing a diverse array of banking and financial services to consumers, small businesses, corporations, and institutions. As investors look to navigate the complexities of the market, understanding the trajectory of key financial stocks like TFC becomes paramount. This comprehensive analysis delves into Truist Financial’s historical stock performance, examines the multifaceted factors influencing its valuation, and provides a detailed outlook based on algorithmic price predictions for both the short and long term. With a current price of $38.97 USD, the journey of TFC’s stock is intricately linked to macroeconomic forces, sector-specific challenges, and the company’s strategic execution.

A Deep Dive into Truist Financial Corporation (TFC)

Truist Financial was established through a historic merger completed in December 2019, combining two venerable institutions, BB&T and SunTrust, each with over a century of banking heritage. This union created a financial powerhouse with a substantial footprint across the Southeastern and Mid-Atlantic United States. The company’s operations span several key segments: Consumer Banking and Wealth, Corporate and Commercial Banking, and Insurance Holdings. Within these segments, Truist offers a wide range of products and services, including traditional deposit and lending services, credit cards, mortgages, wealth management, brokerage services, and corporate and investment banking solutions. The sheer scale and diversified business model of Truist are critical components of its investment profile, offering both resilience and opportunities for growth in varying economic conditions. Its commitment to digital transformation and client-centric solutions positions it as a significant player poised to adapt to the evolving demands of the modern financial services industry.

Historical Performance Analysis: The Last 12 Months of Truist Financial (TFC)

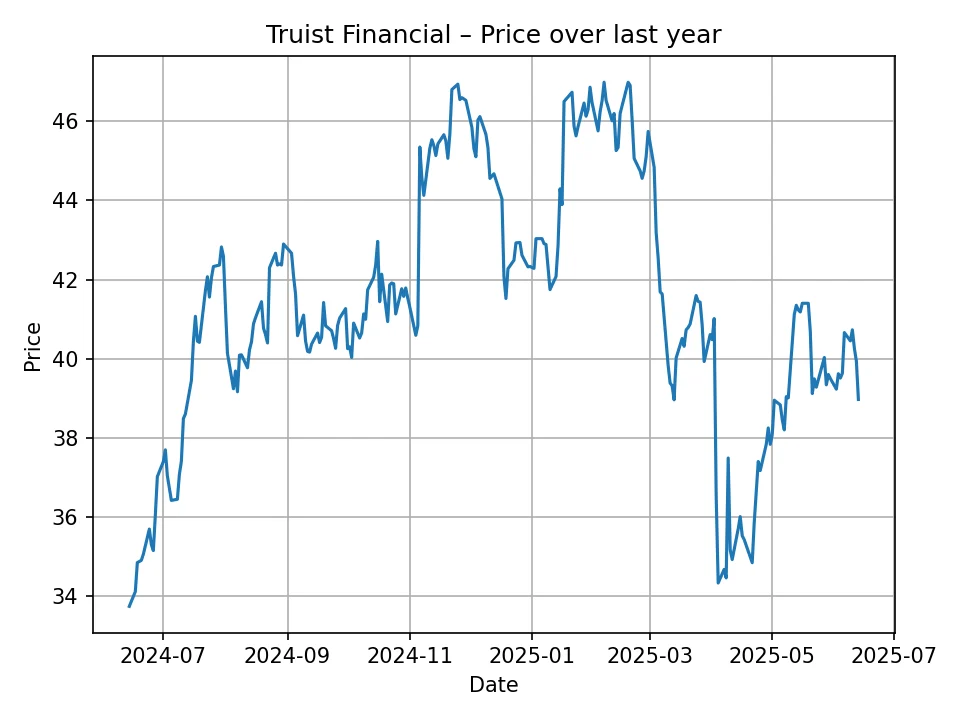

Examining the historical price data for Truist Financial (TFC) over the past 12 months provides invaluable context for understanding its current valuation and potential future movements. The provided daily historical data, spanning from approximately June 2024 back to June 2023, illustrates a journey marked by periods of volatility, growth, and consolidation. Starting from a price point around $33.74 USD, the stock experienced fluctuations, demonstrating the inherent sensitivities of banking stocks to market sentiment and economic indicators. There were instances of significant upward momentum, pushing the price into the high $40s USD and even briefly touching the $46-$47 USD range. These peaks likely coincided with periods of positive economic news, improving interest rate outlooks for banks, or strong corporate performance reports.

Conversely, the data also reveals pullbacks, with prices retreating at various points. For example, after reaching higher levels, the stock often consolidated or experienced corrections, sometimes dropping back into the mid-to-high $30s USD. The most recent price of $38.97 USD positions TFC within the mid-range of its 12-month performance, suggesting that while it has recovered from its lowest points, it still has room to reclaim its previous highs. Factors such as shifts in Federal Reserve interest rate policy expectations, regional banking sector concerns, broader economic growth projections, and Truist’s specific earnings reports and strategic announcements likely played a significant role in shaping these historical price movements. Understanding these past patterns is crucial as it informs expectations for how TFC might react to similar future market conditions and internal developments.

Key Factors Influencing Truist Financial’s Stock Price

The valuation and price trajectory of a financial institution like Truist Financial are influenced by a complex interplay of macroeconomic, industry-specific, and company-specific factors. Investors seeking to understand TFC’s potential must consider these drivers comprehensively.

Macroeconomic Environment and Monetary Policy

- Interest Rates: Perhaps the most significant driver for bank profitability is the interest rate environment. Banks primarily earn money from the spread between what they pay on deposits and what they earn on loans (Net Interest Margin – NIM). Rising interest rates generally lead to higher NIMs, boosting bank earnings, while falling rates can compress them. The Federal Reserve’s monetary policy decisions, including changes to the federal funds rate, directly impact Truist’s profitability. Current and projected interest rate paths are thus critical.

- Inflation: Inflation directly impacts consumer and business spending, loan demand, and operational costs for banks. While moderate inflation can be a sign of a healthy economy, persistent high inflation can lead to aggressive monetary tightening, potentially slowing economic growth and increasing the risk of loan defaults.

- Economic Growth and Recession Risk: A robust economy fuels demand for loans, mortgages, and other financial services, leading to higher revenue for banks. Conversely, an economic slowdown or recession can increase loan defaults, requiring banks to set aside more capital for credit losses, which directly impacts profitability and investor confidence. GDP growth, employment figures, and consumer confidence indices are key indicators.

- Geopolitical Events: Global political instability, trade disputes, and international conflicts can create market uncertainty, affecting investor sentiment and capital flows, which in turn can influence bank stock performance.

Financial Sector Trends and Regulatory Landscape

- Regulatory Changes: The banking sector is heavily regulated. Changes in capital requirements (e.g., Basel III reforms), liquidity rules, consumer protection laws, and stress testing mandates can significantly impact bank operations, profitability, and ability to lend. Stricter regulations often mean higher compliance costs and less financial flexibility.

- Competition: The financial services industry is intensely competitive, not only from traditional banks but also from fintech companies, credit unions, and non-bank lenders. Truist must continually innovate and differentiate its services to retain and attract customers.

- Technological Disruption: The rise of digital banking, mobile payments, and artificial intelligence is transforming the industry. Banks that successfully adopt and leverage new technologies to enhance customer experience, improve efficiency, and reduce costs are better positioned for future growth. Truist’s investment in digital platforms is a key area to monitor.

- Credit Quality Cycles: The health of a bank’s loan portfolio is cyclical. During economic expansions, loan quality generally improves, and defaults decrease. During downturns, non-performing loans rise, leading to higher loan loss provisions and potentially impacting profitability and capital.

Company-Specific Factors

- Earnings Performance: Quarterly and annual earnings reports are crucial. Investors closely scrutinize metrics like Net Interest Income, Non-Interest Income, Net Interest Margin, loan growth, deposit growth, and efficiency ratios. Consistent earnings growth and effective cost management are positive indicators.

- Asset Quality: The quality of Truist’s loan portfolio is critical. High levels of non-performing assets (NPAs) or increased loan loss provisions can signal financial distress and erode investor confidence. Monitoring sectors with higher exposure (e.g., commercial real estate, consumer credit) is important.

- Capital Strength and Liquidity: Regulatory capital ratios (e.g., CET1 ratio) and liquidity levels demonstrate a bank’s ability to withstand financial shocks. Strong capital buffers are reassuring to investors and regulators.

- Management Strategy and Execution: The effectiveness of Truist’s leadership in executing its strategic initiatives, such as digital transformation, cost optimization, market expansion, and cross-selling, directly impacts its long-term growth and profitability.

- Dividend Policy and Share Buybacks: For many investors, particularly those seeking income, a stable or growing dividend is a significant factor. Share buybacks can also enhance shareholder value by reducing the number of outstanding shares and boosting earnings per share.

- Mergers and Acquisitions (M&A): As a product of a large merger, Truist’s ability to successfully integrate acquisitions and realize synergies is critical. Future M&A activity, whether as an acquirer or a target, could also significantly impact its stock price.

Analyzing TFC’s stock requires a holistic view, considering how these interconnected factors evolve and interact within the broader financial and economic landscape.

Fundamentals of Truist Financial

To provide a robust foundation for price predictions, it’s essential to examine the core financial fundamentals of Truist Financial. These elements illustrate the company’s intrinsic value and operational health.

Revenue Streams and Net Interest Margin (NIM)

Truist generates revenue primarily through two main channels: Net Interest Income (NII) and Non-Interest Income. NII is the difference between the interest earned on assets (like loans and investments) and the interest paid on liabilities (like deposits). It is heavily influenced by the volume of loans and deposits, as well as the prevailing interest rate environment and the bank’s Net Interest Margin (NIM). A higher NIM indicates better profitability from core lending activities. Truist aims to optimize its NIM through careful management of its balance sheet, including loan pricing and funding costs.

Non-Interest Income comprises fees and commissions from various services, including wealth management, insurance, corporate and investment banking, treasury services, and service charges on deposit accounts. This diversified stream provides a crucial hedge against interest rate fluctuations and contributes significantly to overall profitability. Truist’s substantial insurance brokerage business, for instance, offers a stable, fee-based income stream that differentiates it from many traditional banks.

Asset Quality and Credit Risk Management

The health of Truist’s loan portfolio is a critical determinant of its financial stability. Asset quality is assessed by examining metrics such as non-performing assets (NPAs), net charge-offs (NCOs), and the provision for credit losses. Truist employs rigorous underwriting standards and risk management practices to mitigate credit risk across its diverse loan portfolio, which includes consumer, commercial, and real estate loans. Economic downturns or sector-specific challenges can lead to an increase in loan defaults, necessitating higher provisions for credit losses, which directly reduce reported earnings. The company’s ability to manage its credit exposure effectively, particularly in segments susceptible to economic cycles, is vital for long-term shareholder value.

Capital Ratios and Regulatory Compliance

Strong capital ratios are paramount for banks, serving as a buffer against unexpected losses and a measure of financial resilience. Regulatory bodies impose stringent capital requirements, such as the Common Equity Tier 1 (CET1) ratio, which measures a bank’s core equity capital against its risk-weighted assets. Truist consistently maintains capital levels well above regulatory minimums, demonstrating its financial strength and ability to absorb potential shocks. Adequate capital also supports organic growth initiatives, dividend payments, and share repurchase programs, all of which are attractive to investors. Liquidity management, ensuring the bank has sufficient cash and easily convertible assets to meet its short-term obligations, is another key aspect of financial health.

Operational Efficiency and Cost Management

Efficiency is a cornerstone of banking profitability. The efficiency ratio, which measures non-interest expense as a percentage of revenue, indicates how effectively a bank manages its operating costs. A lower efficiency ratio generally signifies better cost control. Following the merger, Truist has been heavily focused on realizing synergy savings and optimizing its operational footprint, including branch consolidation and investments in technology. Successful execution of these efficiency initiatives can significantly boost the bottom line and improve investor perception. Digital transformation efforts are a key part of this strategy, aiming to reduce manual processes and enhance customer self-service capabilities.

Shareholder Returns: Dividends and Share Buybacks

Truist has a history of returning capital to shareholders through dividends and, at times, share repurchase programs. A consistent and growing dividend payout makes TFC an attractive option for income-focused investors. Share buybacks can enhance earnings per share (EPS) by reducing the number of outstanding shares, often signaling management’s confidence in the company’s valuation. The ability to maintain these shareholder return policies is dependent on strong profitability and robust capital levels, which are subject to regulatory approval.

In summary, Truist Financial’s fundamentals reflect a large, diversified financial institution with substantial revenue-generating capabilities, a focus on risk management, solid capital foundations, and an ongoing commitment to operational efficiency and shareholder value. These underlying strengths provide the basis for assessing its future performance and price trajectory.

Market Dynamics and Macroeconomic Outlook for Banking Sector

The performance of Truist Financial, like any major bank, is inextricably linked to the broader market dynamics and macroeconomic outlook. Several key themes are shaping the environment in which TFC operates.

The Evolving Interest Rate Environment

As of mid-2025, the interest rate landscape continues to be a focal point for the banking sector. The Federal Reserve’s stance on monetary policy, driven by inflation targets and employment data, directly impacts Truist’s Net Interest Margin (NIM). If inflation pressures subside and economic growth moderates, the Fed might consider rate cuts, which could potentially compress NIMs for banks, although it could also stimulate loan demand. Conversely, if inflation proves stickier or economic growth remains robust, the Fed might maintain higher rates for longer, potentially supporting NIMs but also increasing the risk of an economic slowdown. Truist’s balance sheet sensitivity to interest rates, including its mix of variable-rate and fixed-rate loans and deposits, will determine how effectively it navigates these shifts.

Inflationary Pressures and Economic Growth

Inflation, while showing signs of cooling from its peak, remains a critical factor. Persistent inflation can erode purchasing power, leading to a tightening of consumer spending and potentially higher loan defaults if wages don’t keep pace. However, it can also drive up the value of assets, which could benefit certain bank operations. The overall trajectory of economic growth – whether the economy achieves a “soft landing” or experiences a recession – will profoundly influence loan demand, credit quality, and business confidence. A resilient economy supports strong loan origination and lower loan loss provisions, benefiting Truist’s profitability. Conversely, a significant economic contraction would pose substantial headwinds.

Regulatory Scrutiny and Compliance Costs

The banking sector remains under significant regulatory oversight, with ongoing discussions around capital requirements, stress testing frameworks, and consumer protection. Any new regulations or stricter enforcement could lead to increased compliance costs, impacting banks’ profitability and operational flexibility. Truist, as a systemically important financial institution (SIFI), faces particular scrutiny, requiring substantial resources dedicated to regulatory affairs. Changes in the regulatory landscape, such as revisions to Basel III endgame rules, could either present opportunities or impose challenges for capital allocation and strategic planning.

Competitive Landscape and Digital Transformation

Competition within financial services is intensifying from multiple fronts. Large national and international banks, regional banks, credit unions, and a rapidly expanding ecosystem of FinTech companies are vying for market share. FinTechs, often unburdened by legacy infrastructure, offer agile and innovative digital solutions, forcing traditional banks like Truist to accelerate their own digital transformation efforts. Truist’s ability to invest in and successfully deploy advanced digital platforms, enhance mobile banking experiences, and streamline online services is critical for attracting and retaining customers, especially younger demographics. This involves significant capital expenditure but is essential for long-term competitiveness and efficiency gains.

Credit Market Conditions and Loan Demand

The health of credit markets directly impacts Truist’s lending activities. Factors such as corporate borrowing appetite, consumer confidence for taking on new debt, and the overall availability of credit will dictate loan growth. If economic uncertainty persists, businesses and consumers may become more cautious about borrowing, potentially stifling loan origination. Conversely, a stable or improving economic outlook could unleash pent-up demand for credit, boosting Truist’s loan portfolio. Monitoring delinquency rates and broader credit market indicators provides insights into potential future loan loss provisions.

In essence, Truist Financial’s future performance is heavily reliant on its ability to skillfully navigate these evolving market dynamics. Its diversified business model and strong regional presence provide some resilience, but adaptability to changes in interest rates, economic conditions, and technological advancements will be key to its success.

Price Prediction Methodology

Forecasting stock prices, especially for complex entities like a financial institution, is an intricate endeavor that combines quantitative analysis with an understanding of qualitative factors. While precise future prices are impossible to guarantee, advanced analytical techniques can provide informed projections based on historical data and current market conditions. The forecasts presented in this article for Truist Financial (TFC) have been generated using a proprietary algorithmic model named EdgePredict. This algorithm leverages a sophisticated blend of statistical modeling, machine learning techniques, and time-series analysis to identify patterns and trends within the vast amount of historical price data provided. It aims to capture market dynamics, volatility, and historical correlations to project potential future price points. It’s important to understand that these predictions are a product of data-driven computational analysis and do not account for unforeseen geopolitical events, sudden regulatory shifts, or entirely novel market disruptions that fall outside the historical patterns it learns from. Therefore, while providing valuable insight, all predictions should be viewed as probabilities rather than certainties and used as one component of a broader investment strategy.

Truist Financial (TFC) Price Forecasts

Based on the analysis performed by the EdgePredict algorithm, the following are the projected price ranges for Truist Financial (TFC) over the next 12 months and the next 10 years. These forecasts aim to provide a data-driven perspective on the stock’s potential trajectory.

Monthly Price Forecast for Truist Financial (TFC) – Next 12 Months

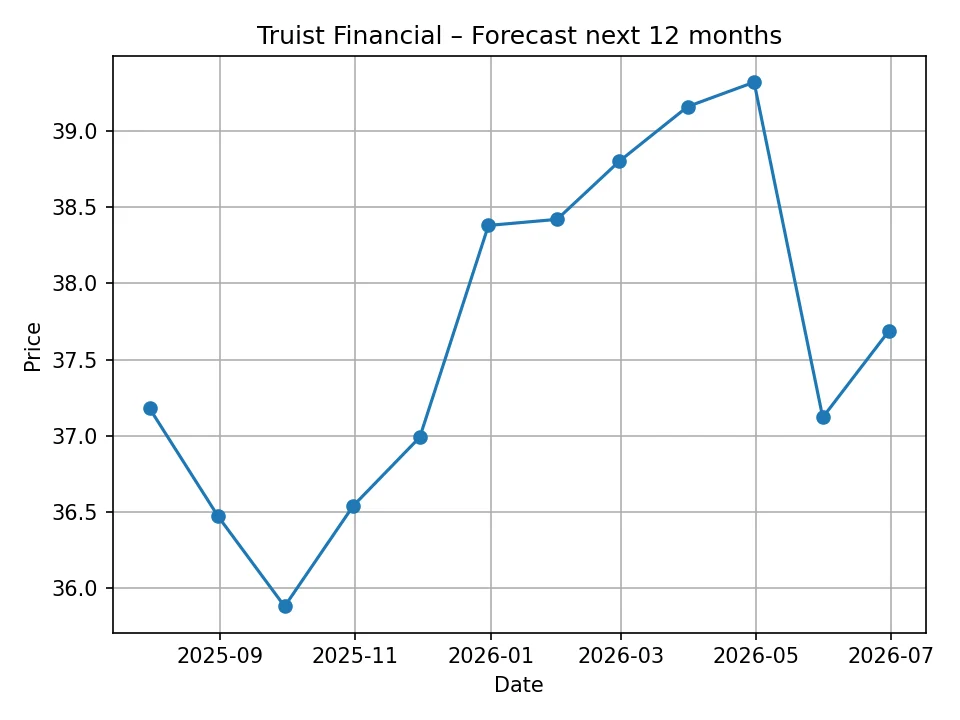

The short-to-medium term outlook for Truist Financial, spanning the next 12 months, suggests a period of potential consolidation followed by a gradual upward trend. The EdgePredict algorithm indicates that TFC may experience some initial downward pressure before finding support and commencing a recovery. This reflects the complex interplay of current economic uncertainties, ongoing banking sector adjustments, and Truist’s internal operational developments.

The forecast suggests that in the immediate months following June 2025, TFC could see a slight dip, possibly reflecting near-term market sentiment or adjustments to economic expectations. However, as the year progresses into late 2025 and early 2026, the algorithm anticipates a slow but steady ascent. This projected recovery could be driven by a stabilization of the interest rate environment, positive developments in Truist’s cost efficiency initiatives, or an improvement in overall credit quality as the economic outlook clarifies. Investors should observe upcoming earnings reports and any strategic announcements from Truist’s management, as these will be critical in confirming or challenging these short-term projections. The table below details the monthly price predictions:

| Month/Year | Projected Price (USD) |

|---|---|

| July 2025 | 37.18 |

| August 2025 | 36.47 |

| September 2025 | 35.88 |

| October 2025 | 36.54 |

| November 2025 | 36.99 |

| December 2025 | 38.38 |

| January 2026 | 38.42 |

| February 2026 | 38.80 |

| March 2026 | 39.16 |

| April 2026 | 39.32 |

| May 2026 | 37.12 |

| June 2026 | 37.69 |

The fluctuations shown in the monthly forecast underscore the ongoing volatility in the financial markets. The expected dip in late summer/early autumn followed by a gradual recovery into the end of the year and early next suggests a market adjusting to new realities, potentially seeing a stronger performance as the economic picture gains clarity. The slight dip again in May 2026 before a rebound in June indicates that while the general trend is upward, short-term pressures can still influence prices.

Annual Price Forecast for Truist Financial (TFC) – Next 10 Years

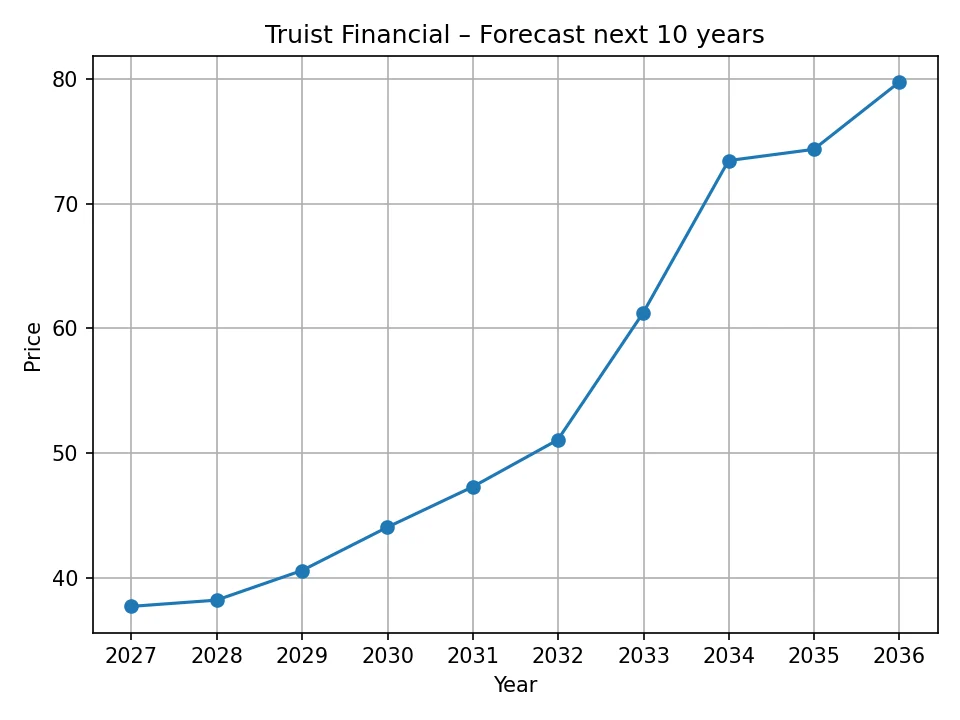

Looking further out, the 10-year annual price forecast for Truist Financial paints a more optimistic picture, projecting significant long-term growth for the stock. This longer-term outlook often discounts short-term market noise and instead focuses on fundamental economic expansion, Truist’s strategic initiatives, and its ability to adapt and grow within the financial sector. The EdgePredict algorithm suggests that after an initial period of more modest growth, TFC’s price could accelerate considerably in the latter half of the decade.

From 2026, where the price is projected to settle at $37.69 USD, the forecast indicates a steady, albeit initially slow, appreciation in value through 2027. This period likely accounts for ongoing post-merger integration, optimization efforts, and gradual economic recovery. However, from 2028 onwards, the projected growth becomes more pronounced, with significant jumps in subsequent years. This acceleration could be attributed to several factors: the full realization of merger synergies, successful digital transformation leading to improved efficiency and customer engagement, sustained economic growth driving higher loan demand and asset quality, and potentially a more favorable interest rate environment for bank profitability over the long run. By 2035, the algorithm predicts Truist’s stock could reach nearly $80 USD, more than doubling its current price. Such substantial long-term growth would signify Truist’s successful navigation of competitive pressures, effective capital deployment, and sustained relevance in the evolving financial landscape. However, it is crucial to remember that long-term forecasts inherently carry a higher degree of uncertainty due to the multitude of unpredictable variables over such an extended period.

| Year | Projected Price (USD) |

|---|---|

| 2026 | 37.69 |

| 2027 | 38.19 |

| 2028 | 40.57 |

| 2029 | 44.04 |

| 2030 | 47.28 |

| 2031 | 51.06 |

| 2032 | 61.28 |

| 2033 | 73.48 |

| 2034 | 74.38 |

| 2035 | 79.77 |

The annual forecast demonstrates a compelling long-term growth narrative for Truist Financial. The jump in 2032 and 2033 is particularly noteworthy, suggesting that the algorithm identifies a period where several growth catalysts might converge, propelling the stock significantly higher. This could be reflective of a mature growth phase for the company within a stable and expanding economic backdrop. Investors considering TFC for a long-term portfolio might find these projections appealing, provided the company continues to execute its strategies effectively and the macroeconomic environment remains supportive.

Potential Risks and Opportunities for Truist Financial

While the forecasts provide a directional outlook, it’s crucial to consider the various risks and opportunities that could either hinder or accelerate Truist Financial’s journey towards its predicted prices.

Risks

- Economic Downturn: A severe recession would significantly increase loan defaults across consumer and commercial portfolios, leading to higher loan loss provisions and reduced profitability.

- Interest Rate Risk: While higher rates can benefit NIM, an aggressive or rapid increase could stifle loan demand or lead to an inverted yield curve, which can pressure bank profits. Conversely, too rapid or deep rate cuts could also compress NIM.

- Intense Competition: Competition from larger national banks, agile regional players, and innovative fintech firms could erode market share, particularly in key lending or deposit segments.

- Regulatory Headwinds: New or stricter regulations regarding capital, liquidity, or consumer protection could impose significant compliance costs and operational constraints.

- Cybersecurity Threats: As a digital-first financial institution, Truist faces continuous and evolving cybersecurity risks. A major data breach or system outage could severely damage its reputation and incur substantial costs.

- Operational Execution Risk: Failure to fully realize the synergies from the BB&T/SunTrust merger or to effectively execute its digital transformation strategy could impact efficiency and profitability targets.

- Commercial Real Estate Exposure: Many banks, including Truist, have significant exposure to commercial real estate. A downturn in this sector, particularly in office or retail segments, could lead to increased defaults and losses.

Opportunities

- Economic Recovery and Growth: A sustained period of economic growth would drive increased loan demand, higher consumer spending, and improved credit quality, all benefiting Truist.

- Effective Digital Transformation: Successful implementation of its digital strategy could lead to enhanced customer experience, greater operational efficiency, and a competitive advantage in attracting tech-savvy customers.

- Strategic Market Positioning: Truist’s strong regional presence in growing Southeastern and Mid-Atlantic markets provides a demographic tailwind for deposit and loan growth.

- Cross-Selling Opportunities: Leveraging its diversified business segments (banking, wealth management, insurance) to cross-sell products and services to existing customers can boost non-interest income and deepen client relationships.

- Niche Market Expansion: Identifying and expanding into profitable niche markets or underserved segments could provide new avenues for growth.

- Dividend Appeal: Maintaining a strong and consistent dividend yield can continue to attract income-focused investors, providing a floor for the stock price during volatile periods.

- Disciplined Capital Management: Prudent capital allocation, including strategic investments, organic growth support, and judicious share buybacks, can enhance long-term shareholder value.

Monitoring these factors is essential for any investor considering a position in Truist Financial, as they represent the most significant potential influences on its future performance.

Conclusion

Truist Financial (TFC) stands as a formidable force in the U.S. banking sector, a result of a transformative merger that created a diversified financial services powerhouse. Its journey over the past 12 months has shown periods of both upward momentum and consolidation, reflecting the dynamic nature of the financial markets and the broader economic landscape. The factors influencing its stock price are multifaceted, ranging from the intricate details of interest rate policy and economic growth to company-specific operational efficiency and strategic execution.

The analysis of Truist’s fundamentals reveals a company with robust revenue streams, a focus on asset quality, strong capital positions, and an ongoing commitment to efficiency and shareholder returns. These underlying strengths provide a solid foundation for its future outlook. The price forecasts, generated by our proprietary EdgePredict algorithm, suggest a nuanced short-term path with potential for minor dips and subsequent recovery, followed by a more compelling long-term growth trajectory over the next decade. While the short-term monthly predictions indicate some volatility and a period of initial adjustments, the annual forecasts point towards substantial appreciation, potentially seeing the stock approach the $80 USD mark by 2035. This long-term optimism is predicated on the assumption of continued economic stability, successful strategic implementation by Truist’s management, and effective navigation of regulatory and competitive challenges.

However, it is crucial for investors to remember that these forecasts are based on algorithmic models and historical data, and as such, they are subject to inherent uncertainties. Unforeseen market shifts, significant economic downturns, or dramatic changes in the regulatory environment could impact these projections. As with all investment decisions, prospective and current investors should conduct their own thorough due diligence, consider their individual risk tolerance, and consult with a qualified financial advisor before making any investment choices concerning Truist Financial or any other security.

Disclaimer: The price predictions provided in this article for Truist Financial (TFC) are generated by an independent, proprietary algorithmic model (EdgePredict) and are based on historical data and current market conditions. These forecasts are for informational purposes only and do not constitute financial advice or a recommendation to buy, sell, or hold any security. Stock price predictions are inherently uncertain and subject to market volatility, economic changes, and unforeseen events. We are not responsible for any investment decisions made based on the information presented herein. Investors should conduct their own research and consult with a financial professional before making any investment decisions.

Sophia Patel brings deep expertise in portfolio management and risk assessment. With a Master’s in Finance, she writes practical guides and in-depth analyses to help investors build and protect their wealth.